Ending inventory was made up of 75 units at $27 each,and 210 units at $33 each, for a total FIFO perpetual endinginventory value of $8,955. The specific identification method of cost allocation directlytracks each of the units purchased and costs them out as they aresold. In this demonstration, assume that some sales were made byspecifically tracked goods that are part of a lot, as previouslystated for this method. For The Spy Who Loves You, the first saleof 120 units is assumed to be the units from the beginninginventory, which had cost $21 per unit, bringing the total cost ofthese units to $2,520. Once those units were sold, there remained30 more units of the beginning inventory. The second sale of 180 units consistedof 20 units at $21 per unit and 160 units at $27 per unit for atotal second-sale cost of $4,740.

Physical Count:

This can be obtained from the previous period’s ending inventory or by conducting a physical count at the beginning of the period. The specific identification method involves individually claiming the making work pay tax credit identifying and tracking the cost of each item in inventory. This method is typically used for high-value or unique items where it is practical to track their specific costs.

- However, costs such as freight charges and insurance are usually small, and the cost of trying to allocate them to individual items outweighs the benefit.

- This count can take more than a day and often requires the firm to cease operations.

- These UPC codes identify specific products butare not specific to the particular batch of goods that wereproduced.

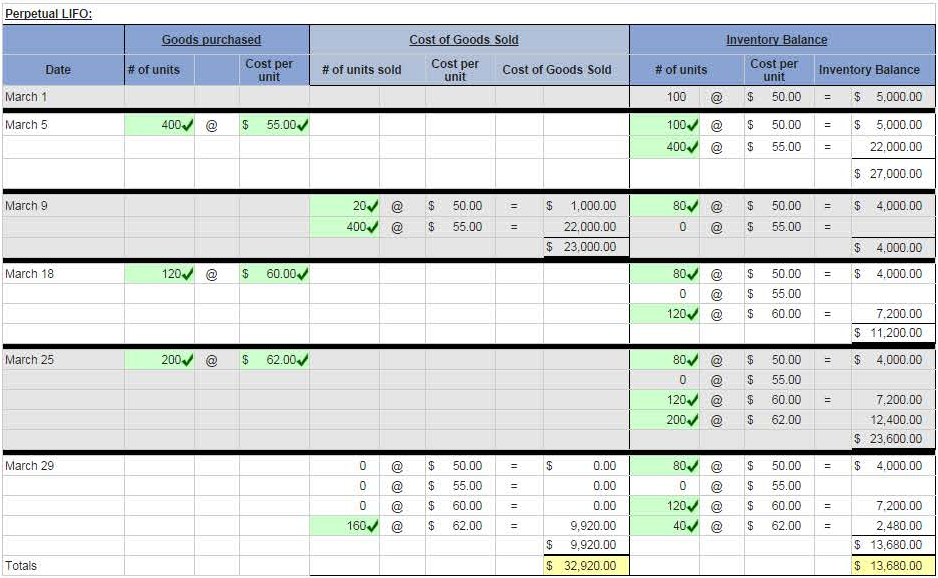

- Cost of goods sold was calculated to be $7,200, which should be recorded as an expense.

- Ending inventory was made up of 75 units at $27 each, and 210 units at $33 each, for a total FIFO perpetual ending inventory value of $8,955.

Calculations for Inventory Purchases and Sales during the

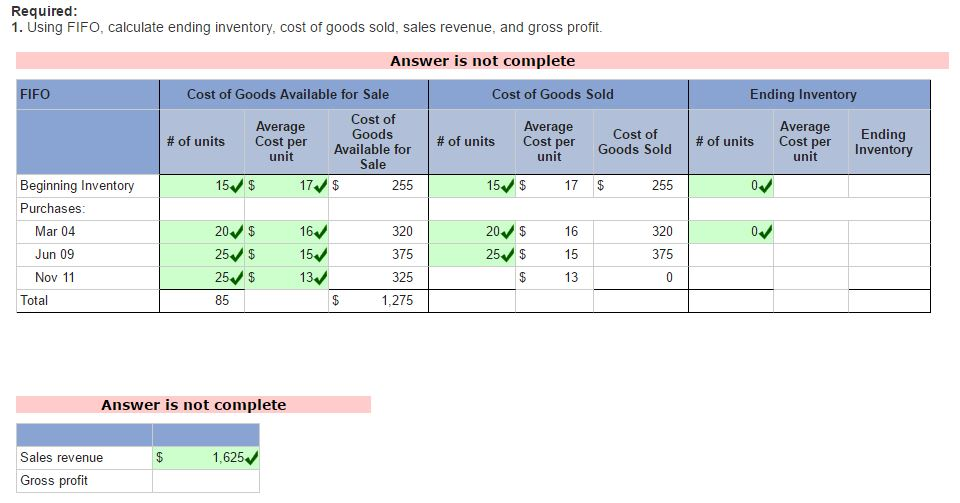

Ending inventory, also known as closing inventory, refers to the total value of goods that a company has available for sale at the end of an accounting period. It is a key component in the calculation of the cost of goods sold (COGS) and is essential for determining a company’s profitability. The value of ending inventory can be calculated using different methods, such as the first in, first out (FIFO), last in, first out (LIFO), and weighted-average cost methods. The inventory at period end should be $7,872, requiring an entry to increase merchandise inventory by $4,722.

Information Relating to All Cost Allocation Methods, but Specific to Periodic Inventory Updating

The inventory valuation method chosen by management impacts many popular financial statement metrics. Inventory-related income statement items include the cost of goods sold, gross profit, and net income. Current assets, working capital, total assets, and equity come from the balance sheet. All of these items are important components of financial ratios used to assess the financial health and performance of a business.

Figure 10.16 shows the gross margin, resulting from the FIFO perpetual cost allocations of $7,200. In this article, the use of LIFO method in periodic inventory system is explained with the help of examples. To understand the use of LIFO in a perpetual inventory system, read “last-in, first-out (LIFO) method in a perpetual inventory system” article. Determining the actual quantity of items in the ending inventory usually requires a physical count.

Average costing method

Merchandise inventory (or inventory) is the quantity of goods available for sale at any given time. The purchases costs, which include the purchase price less any sales discounts, insurance in transit, freight charges, and taxes are included in the ending inventory along with other related direct costs. These costs are added to the total cost of the goods available for sale (the beginning inventory). The cost of ending inventory is determined by accounting for the acquisition costs of each item in the ending inventory. In other words, the problem is how an accountant can determine the acquisition cost or price paid for each item in the ending inventory when the items have been purchased at different times for different prices.

This average cost is then used to assign costs to both the cost of goods sold and the ending inventory. The gross profit method is a technique used to estimate the cost of ending inventory. It involves calculating the gross profit ratio by dividing the gross profit by net sales.

In LIFO periodic system, the 120 units in ending inventory would be valued using earliest costs. Under last-in, first-out (LIFO) method, the costs are charged against revenues in reverse chronological order i.e., the last costs incurred are first costs expensed. In other words, it assumes that the merchandise sold to customers or materials issued to factory has come from the most recent purchases.

However, prices do not remain stable, and so accountants have developed alternative methods to attach costs to inventory items. After the quantity of items is determined, a particular cost flow pattern is assumed, and prices are attached to each item in the inventory. The total of the prices times the quantity equals the cost of the ending inventory. The LIFO method assumes that the inventory items that enter the system last are the first ones to be sold.

Consequently, the costs assigned to the latest units are charged to the cost of goods sold. Figure 10.20 shows the gross margin, resulting from theweighted-average perpetual cost allocations of $7,253. Figure 10.12 shows the gross margin resulting from the weighted-average periodic cost allocations of $8283. Figure 10.20 shows the gross margin, resulting from the weighted-average perpetual cost allocations of $7,253.

However, imagine a firm that sells identical products, such as molded plastic chairs, that have been purchased at different prices. However, costs such as freight charges and insurance are usually small, and the cost of trying to allocate them to individual items outweighs the benefit. When the ending inventory is counted, the firm must ensure that all the items to which it has legal title are part of the count, including goods stored in public warehouses and goods in transit. When valuing ending inventory, it is important to consider the lower of cost or market rule. This rule states that inventory should be valued at the lower of its acquisition cost or market value minus any selling costs. It is essential to report ending inventory accurately, especially when obtaining financing.